It has been a year since the National Bank ceased to manage the tenge exchange rate, and a year since the initial strong devaluation that extended until the end of last year.

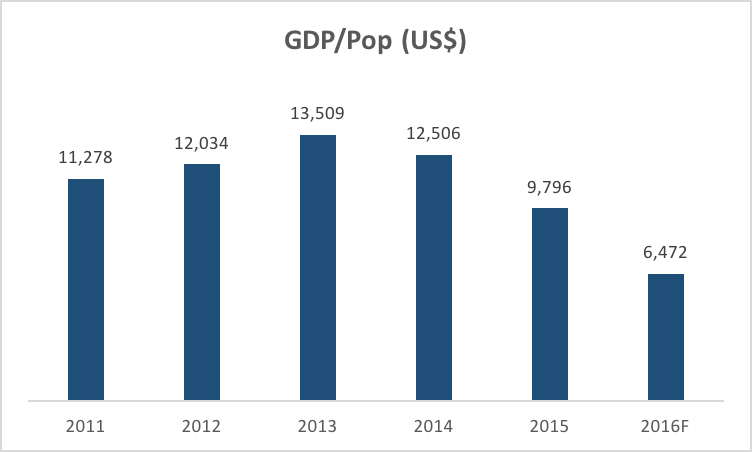

Given the huge loss of purchasing power of the population - GDP per capita is forecasted to have fallen 52% from 2013 to 2016 when measured in US$ - many may wonder if it was the correct decision.

I have written before about the “Trilemma”, or what governments decide to control when they can only control two out three at a time of Exchange Rates, Interest Rates and Capital Flows. The decision to allow the free float became inevitable with the sharp fall in commodity prices that started in the middle of 2014. Not allowing the tenge to devalue would have led to either large capital outflows, or interest rates that would have chocked the economy.

The real issue is when it should have been done, and here it is certain that it was done when there was no alternative, rather than when the economy was still healthy. The desperation measure led to desperate circumstances for large parts of the domestic economy and for parts of the population. The shock led to a huge switch to USD deposits in banks and a severe scarcity of tenge liquidity, which led to a breakdown in payment cycles from which the economy is still trying to recover.

A free float imposes a discipline and a loss of control that many in government may want to avoid, unless forced. That said, adoption during “good times” would have led to less shock to the population and to corporates, and it may be that the absolute lows experienced by the currency, and the disruption in the economy could have been avoided.

The Government is fairly good at protecting the poorer segments of the population, and the wealthy may be relatively immune. However, for the second time in a decade, the nascent middle class is the one that suffers. While they may not be the largest part of the population, they are the backbone to the Nation’s vision of becoming a modern and competitive economy.

No one likes bad news, but those who advise leaders should realise that bad news delayed is usually bad news multiplied. Higher oil prices are not something that policy makers should rely on, the policy makers need to make the economy attractive for the domestic middle class, otherwise all efforts to attract foreign investors could disappoint.

Given the huge loss of purchasing power of the population - GDP per capita is forecasted to have fallen 52% from 2013 to 2016 when measured in US$ - many may wonder if it was the correct decision.

I have written before about the “Trilemma”, or what governments decide to control when they can only control two out three at a time of Exchange Rates, Interest Rates and Capital Flows. The decision to allow the free float became inevitable with the sharp fall in commodity prices that started in the middle of 2014. Not allowing the tenge to devalue would have led to either large capital outflows, or interest rates that would have chocked the economy.

The real issue is when it should have been done, and here it is certain that it was done when there was no alternative, rather than when the economy was still healthy. The desperation measure led to desperate circumstances for large parts of the domestic economy and for parts of the population. The shock led to a huge switch to USD deposits in banks and a severe scarcity of tenge liquidity, which led to a breakdown in payment cycles from which the economy is still trying to recover.

A free float imposes a discipline and a loss of control that many in government may want to avoid, unless forced. That said, adoption during “good times” would have led to less shock to the population and to corporates, and it may be that the absolute lows experienced by the currency, and the disruption in the economy could have been avoided.

The Government is fairly good at protecting the poorer segments of the population, and the wealthy may be relatively immune. However, for the second time in a decade, the nascent middle class is the one that suffers. While they may not be the largest part of the population, they are the backbone to the Nation’s vision of becoming a modern and competitive economy.

No one likes bad news, but those who advise leaders should realise that bad news delayed is usually bad news multiplied. Higher oil prices are not something that policy makers should rely on, the policy makers need to make the economy attractive for the domestic middle class, otherwise all efforts to attract foreign investors could disappoint.

RSS Feed

RSS Feed