The current management of the tenge exchange rate is having a significant impact on the banking sector and the availability of credit. One assumes that this, combined with continued weak oil prices, will translate into very weak economic performance.

Credit to the economy underpins most economies’ ability to grow, but the current defense of the tenge exchange rate makes the biblical maxim come to life. As of May, loans have declined by 1.9% year-on-year, with Corporate and SME loans declining by 3.2% and consumer loans growing by 0.7%. This compares with double digit growth seen in both segments over the past three years. Tenge financing has grown by 5.6%, while foreign currency financing has shrunk by 16.1%. Short term credit is the segment that has suffered the most, with a decline of 6.8%.

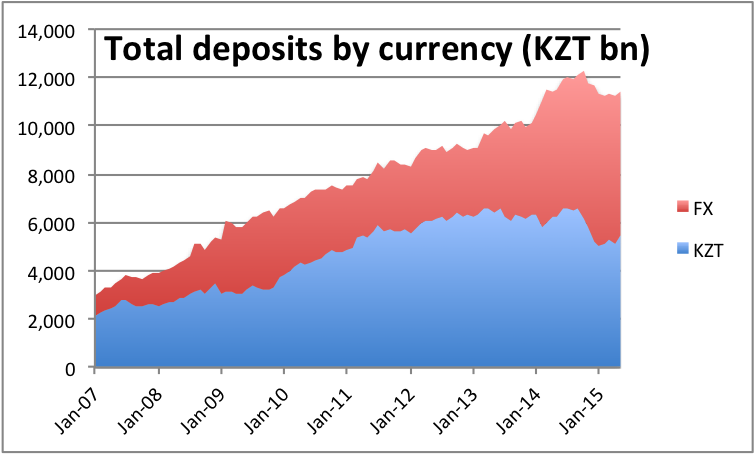

The deposit scenario is not much better. Total deposits have declined by 0.7% year-on-year, with a 12.7% decline in tenge deposits and a 13.6% increase in foreign currency deposits. Deposits are 52% in foreign currency, which makes it difficult for banks to lend, as they do not have access to long term tenge-dollar swaps. Consumer deposits are 68% in foreign currency, while corporates deposits are 43% in foreign currency - reflecting their business needs for local currency and the fact that state owned enterprises dominate the corporate deposit market.

While the IMF official may be correct in his recent statement that the National Bank has the resources to defend the tenge for years, it is not clear if the economy and the banking sector have the same potential resilience. While those with the power to decide may prefer to avoid devaluation, as it looks like a loss of face towards the population and may lead to further declines in local currency deposits, the question is whether it is better to slowly strangle the economic potential of the country and damage the banking sector - which should underpin future economic growth. Hoping for a return to stronger oil prices and Russian ruble is an ephemeral hope, as oil prices have resumed a downward trend, declining about 16%% since early May, and the ruble has declined by almost 17% against the US dollar since mid-May.

One would also assume that, under the current currency exchange rate management, the target for significant reduction in non-performing loans in the banking sector will not be achieved by improving banking sector performance.

There are no easy solutions but, ignoring the problem surely is not one of them.

Credit to the economy underpins most economies’ ability to grow, but the current defense of the tenge exchange rate makes the biblical maxim come to life. As of May, loans have declined by 1.9% year-on-year, with Corporate and SME loans declining by 3.2% and consumer loans growing by 0.7%. This compares with double digit growth seen in both segments over the past three years. Tenge financing has grown by 5.6%, while foreign currency financing has shrunk by 16.1%. Short term credit is the segment that has suffered the most, with a decline of 6.8%.

The deposit scenario is not much better. Total deposits have declined by 0.7% year-on-year, with a 12.7% decline in tenge deposits and a 13.6% increase in foreign currency deposits. Deposits are 52% in foreign currency, which makes it difficult for banks to lend, as they do not have access to long term tenge-dollar swaps. Consumer deposits are 68% in foreign currency, while corporates deposits are 43% in foreign currency - reflecting their business needs for local currency and the fact that state owned enterprises dominate the corporate deposit market.

While the IMF official may be correct in his recent statement that the National Bank has the resources to defend the tenge for years, it is not clear if the economy and the banking sector have the same potential resilience. While those with the power to decide may prefer to avoid devaluation, as it looks like a loss of face towards the population and may lead to further declines in local currency deposits, the question is whether it is better to slowly strangle the economic potential of the country and damage the banking sector - which should underpin future economic growth. Hoping for a return to stronger oil prices and Russian ruble is an ephemeral hope, as oil prices have resumed a downward trend, declining about 16%% since early May, and the ruble has declined by almost 17% against the US dollar since mid-May.

One would also assume that, under the current currency exchange rate management, the target for significant reduction in non-performing loans in the banking sector will not be achieved by improving banking sector performance.

There are no easy solutions but, ignoring the problem surely is not one of them.

RSS Feed

RSS Feed